The Medicare Payment Advisory Commission (MedPAC) paints a rosy portrait of home health margins. But an analysis of cost reporting data – that considers both traditional Medicare and Medicare Advantage (MA) payments – shows that providers are generally not sitting atop a hill of money. Instead, they are struggling to stay above water.

Kalon Mitchell sold his company to the post-acute technology organization WellSky in 2018. He then worked for WellSky for five more years, learning the ins and outs of the home health industry in the meantime.

After leaving WellSky, and with some more time on his hands, Mitchell decided to start “Project Sword”, which leverages cost reporting data to analyze the financial position of home health providers at large.

The data shows not an industry enjoying close to 20% margins, but instead one that is in a deeply precarious position moving forward.

The Centers for Medicare & Medicaid Services (CMS) has proposed cuts to home health payments three years in a row. Though its last two final payment rules have not been as harsh as its proposals, they have still come with permanent cuts to payments.

Providers have multiple gripes with these cuts. The first is over the payment methodology that CMS applies, which most providers and advocates strongly disagree with. The second is the rising costs that home health agencies have recently faced. While CMS is cutting home health payment in traditional Medicare, the cost of providing services has skyrocketed – namely due to the cost of labor.

But the final gripe is the one that has turned into a “generational battle” for providers, and that is MA penetration and payment.

Over 50% of Medicare beneficiaries are now under an MA plan, and those plans generally pay far less for home health care than traditional Medicare.

Providers have regularly told Home Health Care News that MA payment for home health services doesn’t cover the cost of delivering care. But providers tend to be mission driven, and also have referral relationships to uphold. Therefore, they continue to take on MA patients, which sinks their overall margins.

Essentially, traditional Medicare subsidizes MA plans in home health care. It’s true that if providers only took traditional Medicare, they would likely enjoy healthy margins. On the other end, though, if they only took MA, they’d likely have inoperable businesses.

While providers have shared these MA payment horror stories anecdotally, it’s been hard to get a good overall picture of what the average home health provider’s margin looks like of late – as both MA penetration and traditional Medicare rate cuts continue unabated.

The whole picture

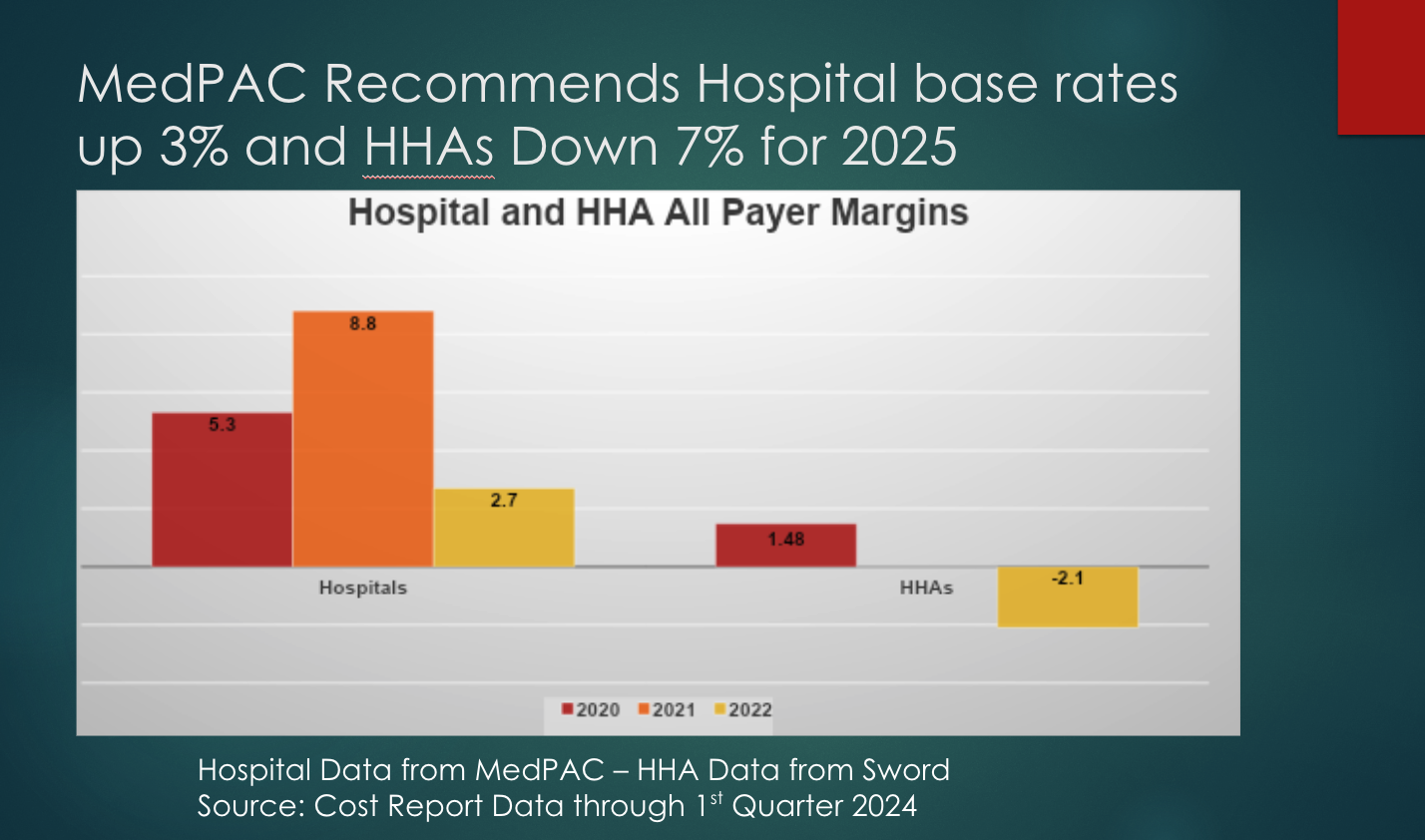

Whereas traditional Medicare subsidizes MA in home health care, the opposite dynamic exists for hospitals.

MedPAC has repeatedly said that it can only consider Medicare payments when analyzing the home health industry.

“The Commission’s review indicates that FFS Medicare’s payments for home health care are substantially in excess of costs,” MedPAC wrote in its March report. “Home health care can be a high-value benefit when it is appropriately and efficiently delivered, but these excess payments diminish that value.”

At the same time, MedPAC includes all-payer data for hospitals in its reports. For instance, it acknowledged that aggregate hospital margins on traditional Medicare had fallen to -11.6% in 2022, while aggregate “all-payer” margins were at about 2.6%.

But in home health care, the other side of the payment picture is not acknowledged.

“In the MedPAC report, they say one of the supposed foundations of what they’re supposed to do is look at all-payer margins,” Mitchell told HHCN. “And in the chapter on home health, there is no mention of all-payer margins.”

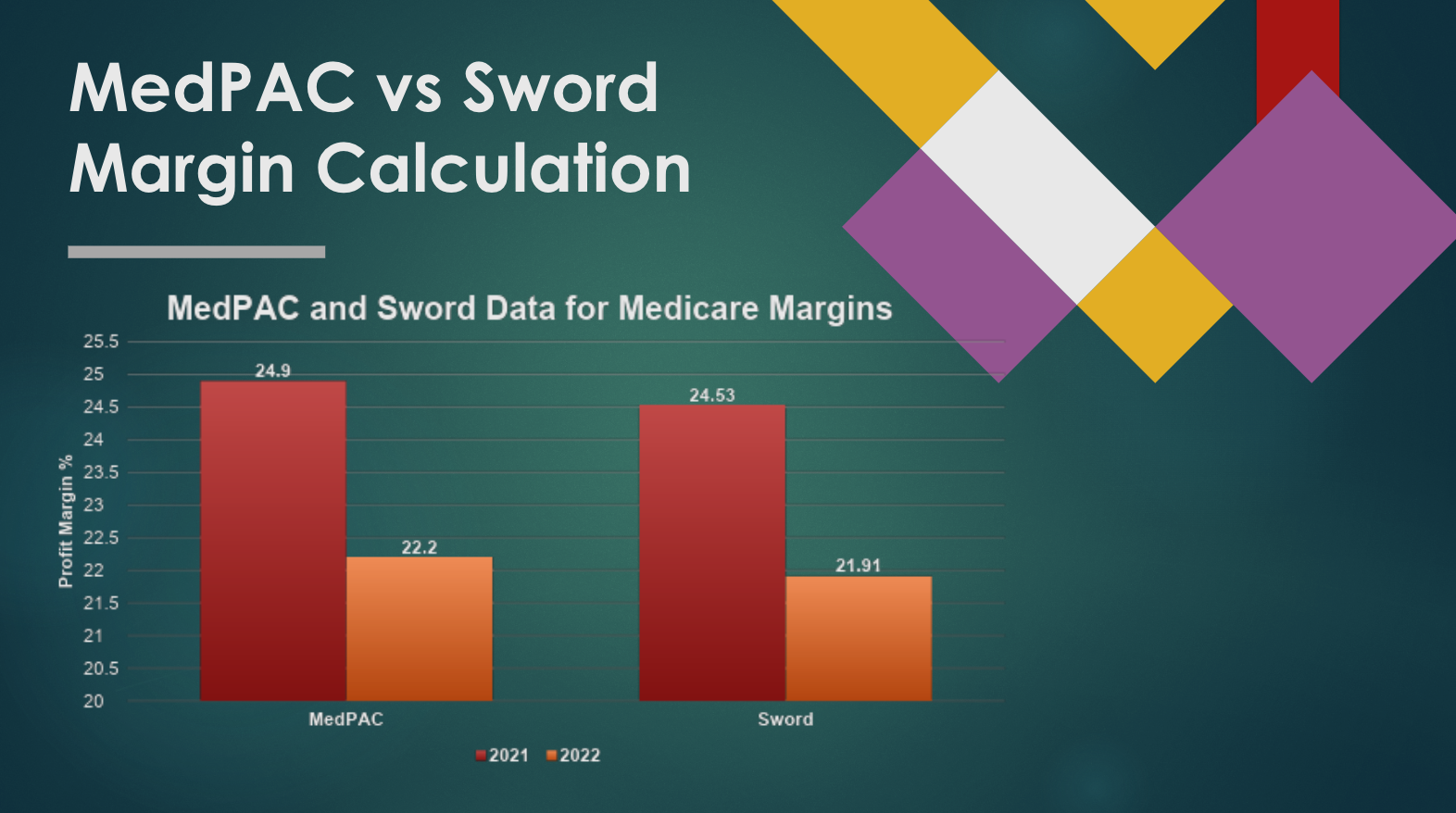

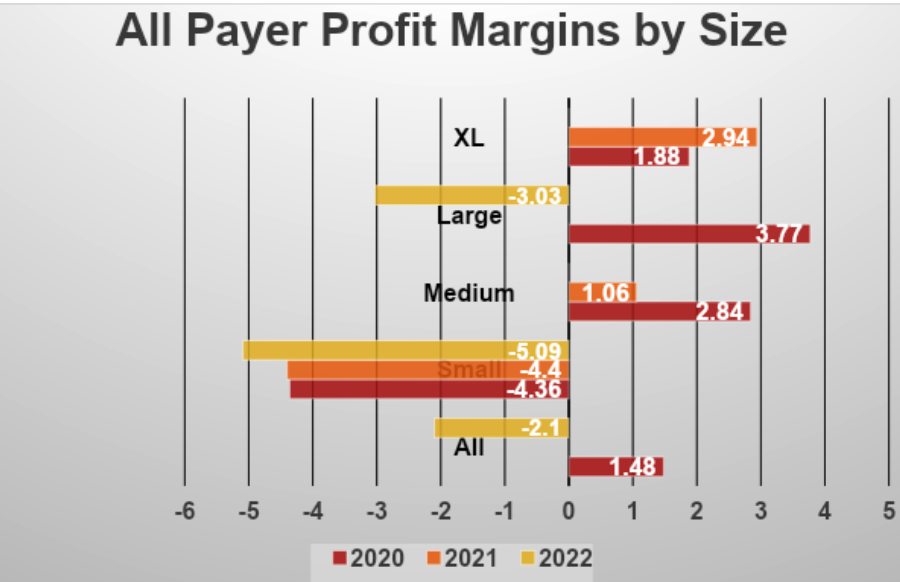

What Mitchell found while working on Project Sword was that MA payments were erasing the healthy margins that could potentially come with a revenue mix dominated by traditional Medicare.

Project Sword and MedPAC’s analyses spit out similar data for Medicare margins, lending credence to Mitchell’s all-payer margin calculations.

When it came to the all-payer outlook, Mitchell found that home health margins sunk below the break-even point.

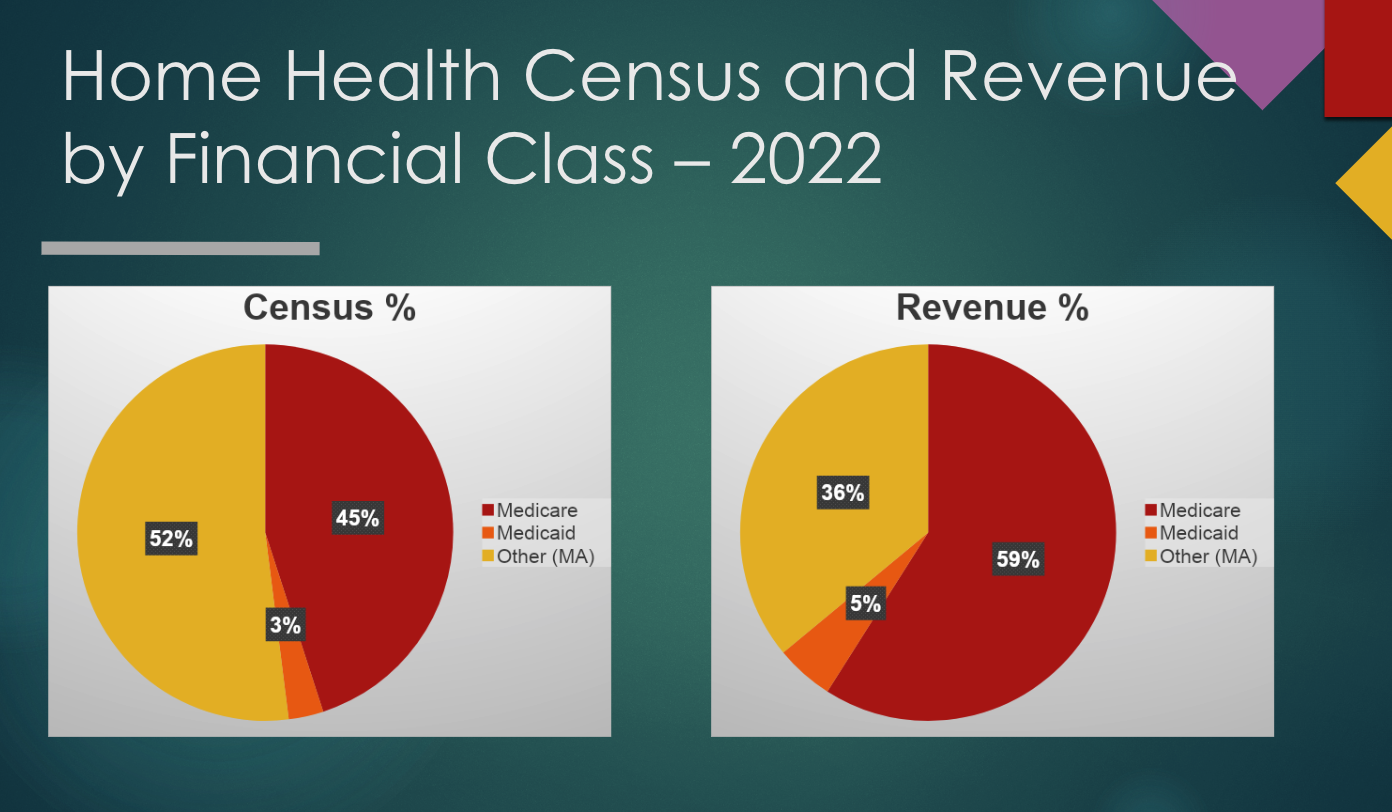

While 59% of home health agency revenue still comes from traditional Medicare, those beneficiaries now account for only 45% patient censuses.

Cost reporting generally lags, which is why much of the data Mitchell used is from 2022.

But since that point, it’s likely that the situation has exacerbated. MA penetration has continued, while CMS has gone through with another payment cut in traditional Medicare.

“We can see a deteriorating industry, and yet the narrative from CMS and MedPAC is that there’s no better industry to be in than home health care,” Mitchell said. “They have the highest profit margins, and that’s what Congress sees when they look at their report. That’s what they hear when they talk to CMS and MedPAC. But when they talk to agencies and advocates, they hear the opposite.”

Mitchell has been cleaning and trimming the data as much as possible to ensure that his project can turn into a meaningful tool for the industry.

Providers have also told him – and HHCN – that the numbers are on par with what they’re seeing internally.

“We want to take care of everybody, but the reality is that the payments we get from fee-for-service Medicare Advantage don’t typically cover our costs,” Michael Johnson, the chief researcher of home care innovation at Bayada Home Health Care, recently told HHCN. “So, we’ve got to make sure we have the right and best mix. That isn’t any different [than in years past], but we have to take even more clarity and focus on that approach now.”

Bayada has been around for nearly 50 years. It also has hundreds of locations, both in the U.S. and abroad.

While the current payment dynamics are tough, the company has the means to survive. It has the means to find a better payer mix, to become more efficient operationally.

Bayada and other larger home health providers also have a chance to get a better deal with MA plans. That could mean a better per-visit rate or some sort of value-based arrangement.

For smaller providers, that’s not the case.

“We have been very selective on what payers that we work with because of this,” LTM Group CEO David Kerns told Home Health Care News. “But I think especially smaller agencies, they may not have a payer innovation team, for instance. We’re not a huge agency, but we do have some scale. For smaller agencies, it’s hard to get payers to even credential your contract, let alone negotiate a value-based arrangement with you.”

As a result, fewer home health providers exist today than five years ago.

In total, there were 11,353 active home health agencies in 2022, 11,474 in 2021, 11,565 in 2020, and 11,569 in 2019, according to the Research Institute for Home Care (RIHC).

Last month, one of the oldest home-based care providers in the country – VNA Of Greater Philadelphia – closed its doors amid “unsustainable financial losses.”

A home health leader recently told Home Health Care News that one of its MA contracts hadn’t been updated for a decade. When it approached the payer about a rate adjustment, the plan offered a $3 increase.

The Preserving Access to Home Health Act of 2023 included a provision that would have forced MedPAC to consider all-payer margins in home health care, but that did not make it through.

So, with MA reimbursement that sometimes only covers a portion of the cost of care, and CMS reducing traditional Medicare rates, providers are left to their own devices to survive.

A closer look at the data

Mitchell is aware that there are errors in the data used for Project Sword. But those errors aren’t necessarily ones that would change the overall story that the data is telling.

“There are errors in the data. And I don’t know how many people, as I’ve worked on this project, have said, ‘You can’t use that data. It’s full of errors,’” Mitchell said. “My reply to that is, MedPAC and CMS are using it, and they’re providing a very limited perspective on what they’re doing.”

Mitchell has also shown his work as much as possible, and has included spreadsheets and his methodologies on his website.

But another area where there are definitely errors are the cost reports themselves. And that, too, could be hurting home health providers.

“I’ve never heard of a single agency that is making sure that every single one of their expenses is on these cost reports,” Kerns said. “They don’t have every little thing on there that should be on there. You need to recognize a lot of those expenses, and really work closely with whoever is doing your cost reports to make sure those are accurate.”

If anything, that would mean that margins are worse off than they’re portrayed in the reports.

“This has been haunting us for years,” Robert Markette, an attorney with the law firm Hall, Render, Killian, Heath & Lyman, previously told HHCN. “The numbers are all over the place. The baseline problem is that we don’t report it accurately because we don’t take cost reporting seriously. We give CMS the ammunition they need to make their argument that we’re being paid too much. When in fact, I think we’re severely underpaid.”

As for Mitchell, he plans to get the data in front of as many stakeholders as possible in the near-term future.

The final payment rule is generally released in late October or early November, but CMS also plans to continue cutting payments in the coming years.

Companies featured in this article:

Bayada Home Health Care, CMS, Kalon BI Consulting, LTM Group, MedPAC