This article is a part of your HHCN+ Membership

Private equity’s influence in home-based care and health care at large has been exaggerated. But the active health care firms still play an important role.

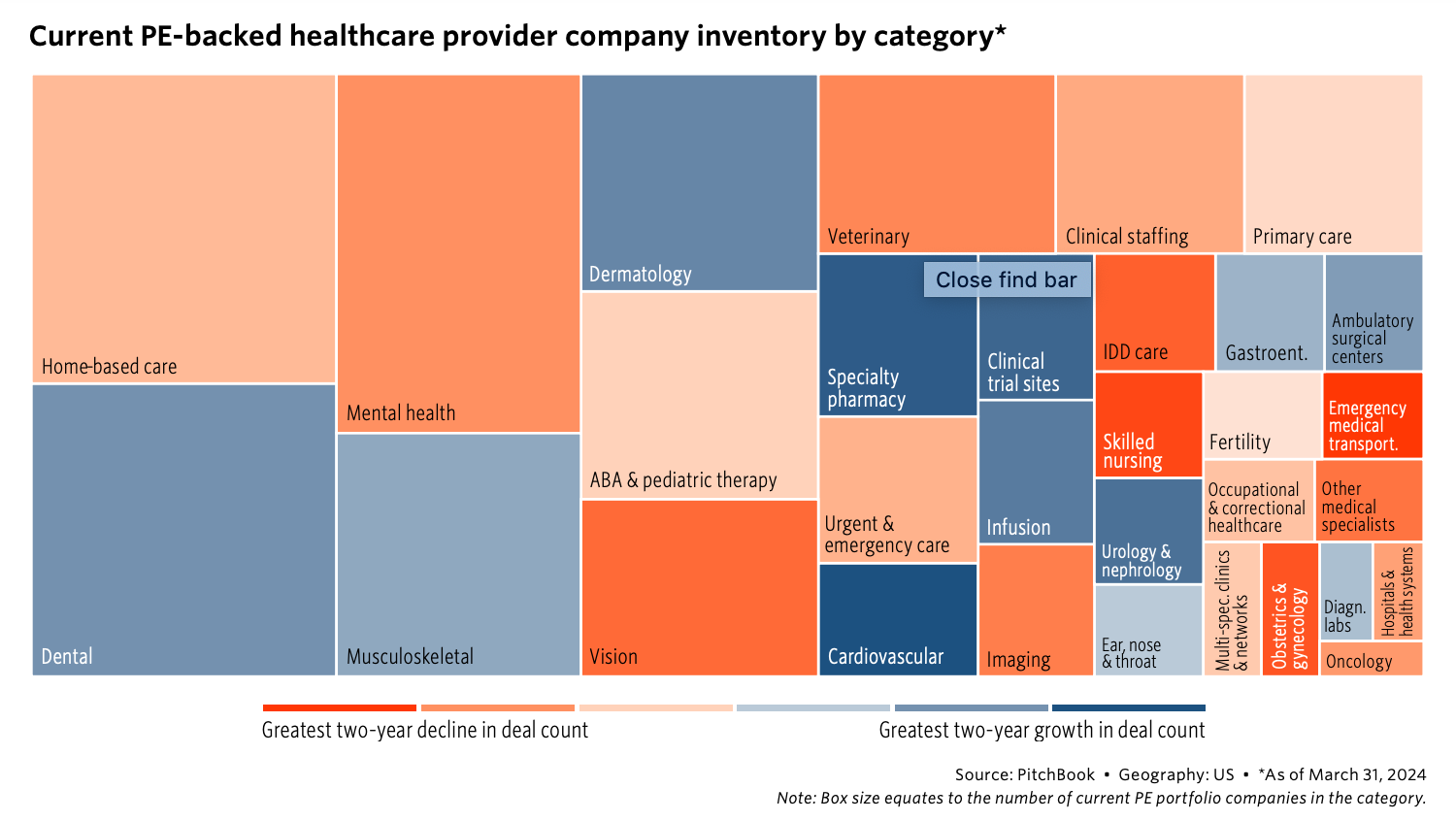

Pitchbook estimates that PE-backed providers represent 3.3% of the U.S. health care provider ecosystem by revenue. There are at least 73 PE-backed home-based care providers, according to Pitchbook, which represents a very small percentage of the thousands of providers out there.

I don’t have the data to back it up, but I would guess that, if insiders and outsiders were polled, their guesses on that first number would come far above 3.3%.

“It’s an estimate. We don’t have disclosed enterprise value and the revenue figures for every company,” Pitchbook Lead Healthcare Analyst Rebecca Springer told me. “But the numbers came out actually a little bit below what I was expecting. And I think it’s a number that’s worth paying attention to.”

Springer and Pitchbook data analysts took a stab at figuring out PE’s control of health care providers “to lay out pertinent, objective information in order to contribute to fact-grounded future discussion.”

The information revealed by Pitchbook this week was eye-opening. I certainly would have guessed that at least 10% of providers had PE backing, for instance.

For the home-based care space in particular, it’s a reminder that PE activity isn’t the end-all, be-all. But it’s also important to remember why PE catches so many headlines in the first place.

In this week’s exclusive, members-only HHCN+ Update, I take a closer look at the relationship between PE, home care and home health care.

Bootstrapping and funding

Pitchbook’s analysis of private equity in health care was not opinionated, and sought out to be exclusively “fact-grounded.”

But the report does come just seven months after the Biden administration released a fact sheet around “promoting competition” in health care to reduce pricing. In that fact sheet, private equity involvement in home care was specifically mentioned as a deterrent to that competition goal.

“Consolidation has also led to a rapid decline in independent physician practices, with research finding that patients of hospital-owned practices pay nearly $300 more for similar care than at independent physician practices,” the fact sheet read. “At the same time, private-equity ownership in the health care industry has ballooned, with approximately $750 billion in deals between 2010 and 2020 — in sectors including, but not limited to, physician practices, nursing homes, hospices, home care, autism treatment and travel nursing.”

The Pitchbook report, on the other hand, showed that 70% of all employed physicians are employed by hospitals; that there has not been a major PE investment in a U.S. hospital or health system since 2018; and that deal activity in both hospitals and skilled nursing facilities is near zero currently.

In home-based care, there was more private equity activity in 2020 and 2021. That’s for two obvious reasons: home-based care is considered a future-facing mode of care, and interest rates at that time – unlike now – were low.

More care will be done in the home in the future given patient preference and cost considerations.

“I think home-based care is a good example of an area that’s attractive to private equity investors because of a high level of fragmentation and demand for increased investment support, scale and increased sophistication on the operating side,” Springer said. “And the long-term tailwind that we see in home-based care, where more patients would like to be treated in the home, where there are cost savings by treating patients in the home.”

That increased level of sophistication is an argument for an influx in PE money being a good thing. For decades, home health care and home care have been mostly dominated by mom-and-pop providers.

Mom-and-pop providers are a must-have, as they often provide care in areas where large companies won’t go. But even some of the more regional providers are just recently turning into more tech-driven operators.

Whereas hospitals were awarded millions to upgrade their EMR systems years ago, for instance, home health providers were awarded nothing.

So, while more patients want to be treated at home than ever, providers are still catching up on the technology side. PE capital gives them the time, money and resources to do so.

That also allows legacy home-based care providers to be the beneficiaries of health care tailwinds, and not new “disruptors” who do have capital and technology, but don’t have experience caring for patients in the home.

It’s also worth noting that a lot of the PE activity in home-based care is through add-ons to existing platforms, or trade-offs from one PE firm to another. In those cases, that’s not “more” PE activity, per se, but just continued PE activity.

The largest deals still usually come from strategics. For instance, UnitedHealth Group’s (NYSE: UNH) $5.4 billion and $3.3 billion deals for LHC Group and Amedisys Inc. (Nasdaq: AMED), respectively.

PE platforms generally look to turn state-wide providers into regional ones, or regional providers into national ones. All things considered, home health agencies gaining more scale is probably a good thing, as home health access remains an issue for Medicare beneficiaries.

The Centers for Medicare & Medicaid Services (CMS) is reducing home health payments by the year. The agency is also scrutinizing profit in home- and community-based services (HCBS), while rate increases remain hard to come by in certain states.

All the while – outside of COVID-19 funding – home-based care providers have been forced to pull themselves up by their bootstraps over the years to modernize. Now, the government has taken some issue with providers looking for outside help via PE.

Currently, 17.3% of GDP spending right now is from health care. Health care’s proportion of PE activity overall is at about 13.8%, according to Springer.

What PE does is help set the standard for industry practices, just like home-based care’s public companies do. That’s why HHCN tracks activity closely. But, as the above numbers show, calling PE involvement in home-based care a concern – even given the bad apples – is probably a bridge too far.

“The deal activity trends in health care broadly mirror what’s going on in the rest of the industries,” Springer said. “There’s been a little bit of variation [over time], but in general, the deal activity remains the same.”